DAAS Built-in strategies

1.Latency – Latency arbitrage is a high-frequency trading strategy based on the latency difference between slow and fast brokers. The software makes trading on slow brokers based on information (quotes update) on the fast brokers. When software catches arbitrage situations (prices on fast and sow brokers are different), the software opens orders on the slow broker, expecting a price change on the slow broker in the same direction in which it happened on a fast broker. For example, the price for EURUSD on a slow broker = 1.34567 on a fast broker 1.34540 Software will sell EURUSD on a slow broker.

2.Lock built-in strategy - Lock allows the software to lock profit on the account and close it by MinTime or MinPips. Detailed description.

3. LockCL's built-in strategy allows the software to lock profit [in the same way as released for the "Lock" build-in strategy], instead of closure, on the same account. The next step for the LockCL algorithm is different from the Lock Algorithm. The software will not close lock by MinTime or MinPips [like what realized it for the “Lock” strategy] but will wait for the next arbitrage situation.

If we have a buy arbitrage signal, the software will close the Sell order from the lock, create a "virtual*" Buy order instead of it, and apply Stop Loss, Trailing Stop, and profit for the "virtual" Buy order. When the close condition is met - it will close the real opened buy order from the lock. If we have a sell arbitrage signal, the soft will close the Buy order from lock and follow the same closing logic.

4. LockCL2's built-in strategy allows the software to lock profit [in the same way as released for the "Lock" build-in strategy], instead of closure, on the same account. The next step for the LockCL2 algorithm is different from that Lock Algorithm. The software will not close lock by MinTime or MinPips [like what realized it for the “Lock” strategy] but will wait for the next arbitrage situation.

If we have a buy arbitrage signal, the software will close the Sell order from the lock, create a "virtual" Sell order instead of it, and apply Stop Loss, Trailing Stop and take profit for the "virtual" Sell order. When the close condition is met - it will reopen real Sell order instead of a virtual one. If we have a sell arbitrage signal, the soft will close the Buy order from lock and follow the same logic.

*- Virtual order - the order exists in the software's memory and follows the program as a real order but does not exist on the server/account.

5. LockCL3'sbuilt-in arbitrage strategy was created to arbitrage on one account and use another only for locking. The software uses Side 2 for arbitrage and Side 1 for locking purposes. It means we will not be searching for arbitrage situations on Side 1.

6. Hedge arbitrage strategy - is a high-frequency trading strategy based on latency difference and liquidity providers quote difference between two or more brokers. When software found the difference, it will open a buy order on the broker with a smaller price and sell order, at the same order size, on the broker with the higher price and wait for the opposite arbitrage situation to close the hedged position.

7.Triangular arbitrage strategy - Triangular arbitrage results from a discrepancy between three foreign currencies, For example, between EURUSD, GBPUSD, and EURGBP, which occurs when the currency's exchange rates do not exactly match up.

8. Statistical arbitrage strategy - Statistical Arbitrage based on the correlation between instruments with historically strong correlation. For example, WTI and Brent, DE30 and F40, Amazon and Apple... Users can pre-define the period for correlation (number of bars for analysis) determination, timeframe, and level for strong correlation. Software sells strong instruments and buys weak instruments when the correlation between them weakens or diverges beyond a pre-defined level. Once mean reversion (or by opposite signal -pre-defined) occurs, the locked position created by the two orders: buy and sell, should generally be in profit. Statistical arbitrage sometimes knows as convergence or pairs trading.

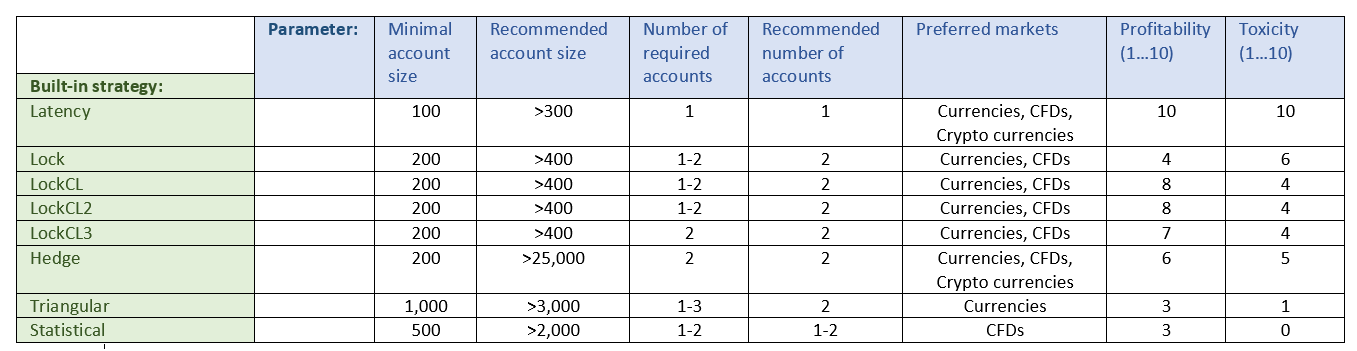

DAAS Built-in strategies comparison table